By David Lukas

If you are a business owner, partner, or independent healthcare professional, you’ve probably felt the sting at tax time. There are many business structures under which you can organize. The two most common are a Limited Liability Company and an S-Corp. Both of these entities are “flow-through” concerning taxation, meaning that all losses and gains of the corporation reflect on your individual tax return. Dollars remaining in the company account at year-end can result in a painful tax liability.

The standard solution most advisors and CPAs advocate is to maximize qualified plan contributions in an attempt to lower the overall tax bill. Unfortunately, these plans have current annual limitations of $18,500 to $55,000 with strict limits on how much you can put aside for yourself.

As a business owner, are you maximizing your qualified retirement plans? Did you know a majority of healthcare business owners are only using 25% of their eligible plan power?

If you are not maximizing your annual contribution, you could be missing out on a significant retirement plan and tax savings opportunity. There is a little-known way to increase your tax-deferred retirement contributions by up to seven times that of a traditional 401(k). Participation could allow contributions of $100,000 per year to $400,000 plus per year.

This “Super 401(k)” allows business owners to maximize the defined-contribution plan up to $55,000, along with a customized defined-benefit program, for a total of $220,000 on average, depending on age, resulting in a total annual contribution of $275,000 per person. This number can be significantly higher if your spouse or another family member is on the payroll.

Because these plans are designed to benefit employers rather than employees, 85% or more of the contribution is retained by you, the business owner. The result? You could realize a significant reduction in your tax bill. For example, with a marginal tax rate of 39.6%, a $300,000 total contribution could yield as much as $118,800 in tax savings! With flexibility in deposits, the plan can be designed to adjust to your business’s annual revenue flow and fiscal calendar for maximum effectiveness.

The Super 401(k) can also include a 401(h) medical expense account, designed to help pay post-retirement medical expenses. The 401(h) permits tens of thousands of dollars of additional savings for future medical expenses in retirement. The 401(h) is the only triple play in the world of tax-advantaged plans because the money put in is pre-tax, it grows tax-deferred, and any withdrawals used for post-retirement medical expenses are free from taxation. The 401(h) account can be used for payment of benefits for hospitalization, sickness, accidents, and medical costs for retired employees, their spouses, and dependents.

Since 1978, the 401(k) has been a benefit for employees, yet has maintained a bias against employers by favoring employees. Savvy employers have the opportunity to cherry-pick the best in pension design with the employees still being cared for, but restoring a bias towards the company owner. The Super 401(k) materially shifts the bias towards employers for key, highly compensated employees. It maximizes the deductibility of owner contributions to retirement benefits while minimizing the plan costs. In many cases, total annual deductions can exceed up to twenty times that of typical qualified plans.

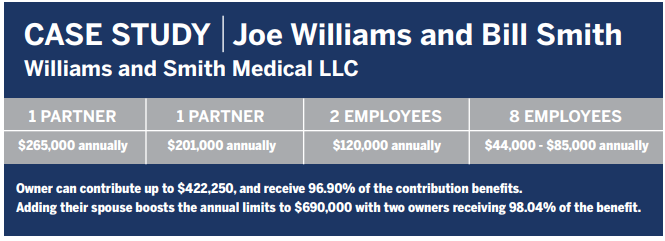

Let’s review a case study to bring it all together. Consider Joe Williams and Bill Smith, the owners of a Medical practice called Williams and Smith Medical LLC. They currently have a store-bought safe-harbor 401(k) in place from a large provider. Williams and Smith Medical LLC have two partners and ten employees. Two partners earning $265,000 and $201,000 per year, two highly compensated employees making $120,000, and eight regular employees with a salary range from $44,000 to $85,000. In this example, the owner using a custom-designed Super 401(k) can contribute not just $18,500 to $24,500, as with a regular 401(k), but over $422,250, and the owners receive 96.90% of the contribution benefits.

Employees still benefit significantly from the addition of a profit sharing plan added to their 401(k). It’s much better than a maximum contribution to a 401(k) only. The owners also have the opportunity to add on their spouses, which boosts the annual limits even more. Now, their medical practice can increase contributions to $690,000 with two owners receiving 98.04% of the benefit.

The Super 401(k) is not a product you buy off the shelf, but a custom-designed retirement plan for business owners, partners, and their employees. Just as an architect creates blueprints for a house or building, an experienced team in this area is a must and will build a custom pension plan and facilitate the conversation necessary with an investment advisor, accountant, and other third parties to ensure compliance with the internal revenue code.

In conclusion, by harnessing the financial benefits of aggregated qualified plans, the Super 401(k) plan design could help you keep more of your hard-earned money and put you on the track to paying fewer taxes and building a multi-million dollar retirement faster than you ever thought possible.

Want to know if the Super 401k Can benefit your business? Call us at 501-218-8880