David Walker. Does that name ring a bell? David Walker served as the comptroller general of the federal government. What does that mean? It means he was the head of the government accountability office. He was the equivalent of the CPA of the United States. He did it for ten years under Bush and Clinton. David Walker took one look at the books, and he said, “Hey, we have promised way more than we can afford to deliver.” He says if you think social security’s terrible; Medicare is five times more expensive.

At 53 trillion dollars of debt, all of the revenue flowing into the US Treasury under today’s tax rates would only be enough to pay the interest payments, Let alone any principal, let alone a single dollar for social security, Medicare, Medicaid, or anything else. David Walker was so concerned about this that in 2008 he resigned and started to crisscross the country raising the warning cry to whoever would listen.

What do MATH and taxes have to do with your retirement and how do you fix this freight train bearing down on your retirement savings? Keep Reading…

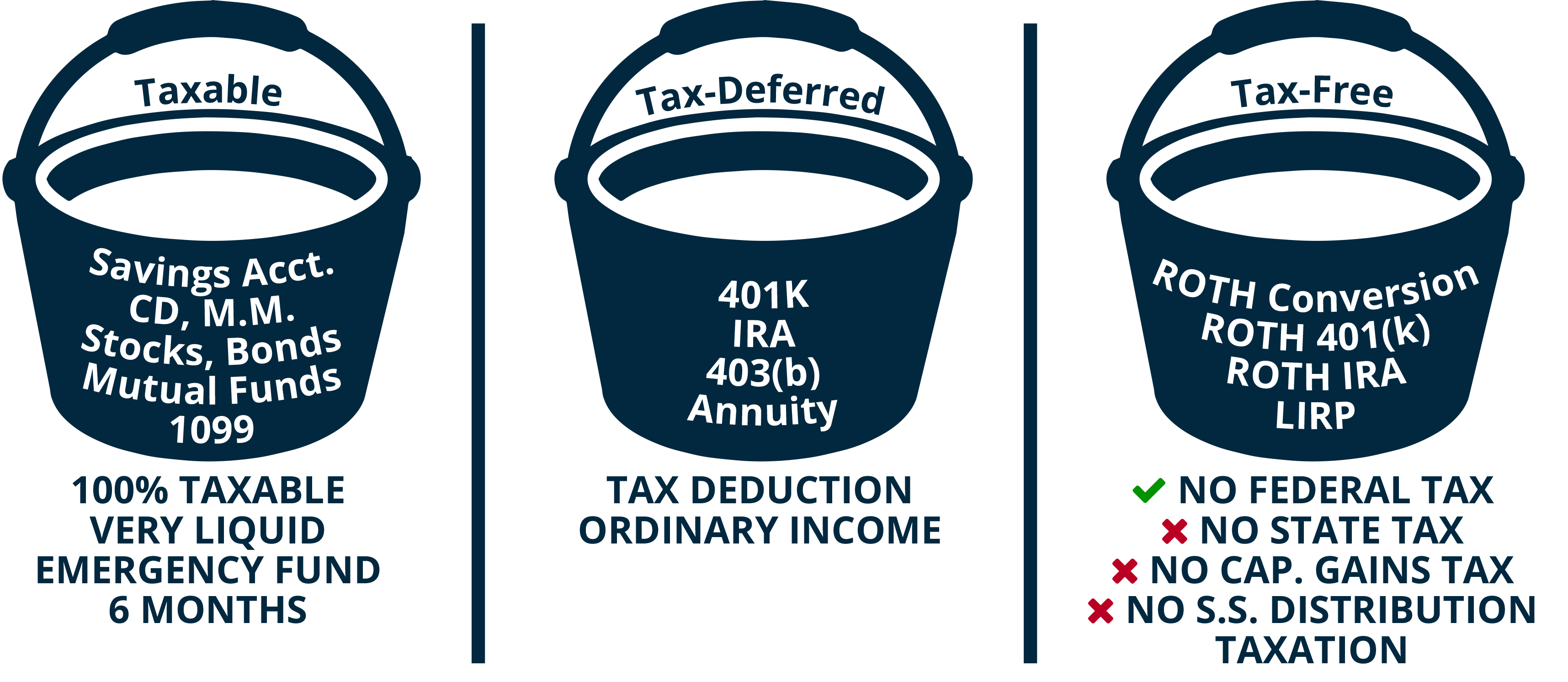

There are all sorts of different ways to save for retirement. There are literally millions of different types of investments out there, however, no matter where you save your money, all of those investments basically fit into only three types of accounts. How’s that for easy?

The first bucket is what we call the taxable bucket, meaning every year as your money grows, you get to pay a tax. At the end of the year, the financial institution sends you a love letter called form 1099. It says, “Your money grew this much and you must give a portion of that money back to the IRS in the form of taxes.” Generally speaking, the growth on the money in this bucket is a hundred percent taxable.

The second bucket is what we call the tax-deferred bucket, meaning you don’t pay taxes on any of those dollars saved until you withdraw the money. The most common tax-deferred account is the 401(k). Other popular accounts in this category include 403(b) and IRAs.

The third Bucket has all sorts of different names. Some people call it tax-advantaged, some call it tax preferred, some call it tax exempt. I call it tax-free. There are all types of different investments out there that masquerade as tax-free, in my opinion, to be truly tax-free, it’s got to qualify in two different ways.The first thing, it’s got to really be tax-free. By tax-free, I’m talking free from three different types of taxes, free from federal tax. Free from state tax, and free from capital gains tax.

The second thing in a true tax-free investment is no social security taxation. In other words, when you take distributions from a true tax-free investment, it should not count as provisional income. Provisional income is the calculation the government uses to determine if up to 85% of your Social Security benefit will be subject to taxes. For an investment to be truly tax-free, It should not count against the threshold which causes social security taxation. When you take interest off your municipal bonds, does that count as provisional income? It sure does. An investment that we’ve been told for years is tax-free doesn’t even meet our two most basic test.

Let’s say tax rates went up to 50% like David Walker’s predicting, how much money would you have to take out of your IRA, be able to pay the 50% tax to the IRS, and then be leftover with $5,000 with which you can then plug the hole in your social security? What’s the double of 5000? $10,000. I bring it up because I’ve done the math 100 times, in 100 different ways and concluded that when your social security gets taxed, you run out of money five to seven years faster than people who do not have their social security taxed. Why? Because the act of compensating for social security taxation forces you to spend down all your other assets that much faster.

The disproportionate amount of people I meet with on a weekly basis have the majority of their savings waiting to be taxed by the government. They have no plan to be in the zero percent tax bracket in retirement. The truth is with proactive tax-planning, it is possible to get into the zero percent tax bracket in retirement and live comfortably. The cost of getting to the 0% tax bracket is you must be willing to pay a tax. In my opinion, given the choice between paying taxes at today’s historically low tax rates or postponing the payment of those taxes until some point much further down the road, you’re probably better off paying them today.

To get into the Zero percent tax bracket in retirement, you’ve got to think beyond working with your CPA, who is typically recording history. Working with an advisor who understands tax-free accumulation and distribution strategies is a must. The combination of the following five strategies can help you achieve the zero percent tax-bracket in retirement.

Contribute no more to your tax-deferred accounts than what will be offset by your standard deductions. This truly is a winning strategy because not only do you get to take a tax deduction on the front end, but you get to spend it tax-free as well!

If your employer offers a ROTH option at work, contribute the maximum amount you can. Even higher income earners who can not contribute to a traditional ROTH can contribute between $18,500 to $24,000 depending on age. If this option isn’t currently available to you, ask for it.

Roth Conversions remain a viable option, although this option has become more tricky with the passage of the Trump tax reform. Be sure to work with someone who knows the rules, or you could get burned.

Number 4

“Back Door Roth Conversions” which allow higher income earners to contribute to ROTH accounts through the “Back Door”. I wrote about this in more detail in the 2017 September-October issue of The Healthcare Journal of Little Rock.

LIRP or Life insurance Retirement Plans (LIRP). This is one of the most misunderstood options among the general population yet one of the most popular among the wealthy and large corporations for tax-free accumulation and distribution. Banks purchased 40-billion dollars of this asset class alone in 2008. For instance, as of 2015 Bank of America Owned 20 Billion in these type of Life insurance retirement plans, yet, Bank of America owned just nine billion in real estate. Industrywide, these type of tax-free savings vehicles dwarfs real estate holdings among the corporations and wealthy.