Do You Have Use and Control of Your Money?

In the first half of life, it is critical that you have liquidity, use and control of YOUR money. The reason so many people in the first half of life fail to save anything substantial is because they have no method to gain use and control of their money during the compounding period. See: Why Compounding Interest Doesn’t Work

In the first half of life, it is critical that you have liquidity, use and control of YOUR money. The reason so many people in the first half of life fail to save anything substantial is because they have no method to gain use and control of their money during the compounding period. See: Why Compounding Interest Doesn’t Work

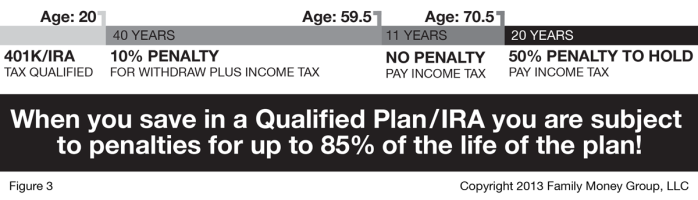

Consider this: With common qualified retirement plans you effectively lock up your money for the next 40 years (assuming you start saving at age 20 – see Figure 3 below). If you do want access to your own money, you are going to pay a 10% penalty (in addition to your regular tax bill) to get to your money. Once you finally reach 59 ½ you enter into a magical eleven-year period where you have access to your money and are not subject to any penalties. During these eleven years, you can take out as much or as little as you wish without the government penalizing you. However, when you turn 70 ½, you are forced to take out what is called a required minimum distribution (RMD). The government wants their fair share. If you don’t take out your RMD, you will be penalized up to a 50% increase in taxes on the money you should have taken out, but didn’t. Now, if you live another 20 years, you are effectively in a penalty phase 80-85% of the time. This poses the question, who as this plan designed for?*

Once you do finally have access to your money without penalty, the rest of that money is yours right? Well, not exactly. You see, you have a partner in your qualified plan: the government. They have essentially put a lien on your plan (postponed taxes). Often times 401k’s and other qualified plans are referred to as “tax-savings plans”. The government knows how to market. In reality they should be called what they really are which are tax-postponement plans. Most people believe they are saving taxes when in reality they are only putting off the inevitable.

If you postpone paying your taxes to a later date, essentially you are subject to a future unknown tax calculation that you have no control over. Only the government decides how much of your money they will let you have. Take a look at USDebtClock.org and decide for yourself if you think taxes are going up, staying the same or going down in the future. If you believe that taxes are going up in the future, then postponing your taxes to a later date is a bad idea.

Contact us for a no cost consultation on how to implement a strategy that provides you:

- Tax-Free Growth

- Tax-Free Distribution

- High Contribution Limits

- Competitive Returns

- Guaranteed Growth

- No risk of investment and interest earned being lost once credited to your contract.

- The ability to self-finance every major purchase through-out your lifetime without ever calling a bank. In other words, you have the ability to borrow against your account at any time (contractually guaranteed) and re-direct those payments back to you. (Minimize Lost Opportunity Cost)

- Leverage an ever increasing pool of capital available for investment opportunities. See: How Banks Make Money You may also wish to listen to David chat with John Moriarty on this subject.

- Loan repayment terms are determined by you. (Unstructured loan payments)

- Earn uninterrupted compounding interest on your money while at the same time maintain complete liquidity, use and control of your money (no 10% penalty for access your money!)

If you are in the 1st half of your life and still actively saving money, you owe it to yourself to stop following the financial herd. A good place to start is to read David’s best-selling book: Book Whose Future Are You Financing?

You can learn more by scheduling a no cost consultation with David by clicking below or call: (501) 218-8880.

Additional Reading and Resources for those in the first half of life: